Application for standard deductions. Child allowance application

Notify the employer in writing by writing a free-form application. The application must be supported by documents confirming the right to tax deduction.

One of the most popular standard deductions is the children's deduction. For the first and second child, an employee can receive a deduction in the amount of 1,400 rubles. for each, for the third and subsequent - 3000 rubles.

In order for the employer to take into account the deductions for children when calculating income tax, he needs to present a document that will serve as the basis. You must write an application and attach to it the birth certificate of each child.

Having received such a statement, the employer will know that before calculating personal income tax, you must first subtract the deductible amount from the accrued salary, income tax is considered from the reduced amount.

VIDEO - Standard deduction per child - Don't miss your benefit!

How to write an application for a standard tax deduction for personal income tax for children?

Like any statement, it must be addressed to a specific person. As a rule, a representative of the management team of the organization always acts as the addressee. Data about the addressee and the applicant are traditionally written in the upper right corner.

Below in the center write the name and title of the form.

The application must include text in which the request is made in the first person for a tax standard deduction for children in certain size. You must specify the exact amount to be deducted.

A list of children and the amount of the corresponding deduction is given. The employee must know that the deduction for the child is only allowed until he reaches the age of majority. If at the same time it continues to study, then the period for granting the deduction is extended to 24 years.

In order to support the ongoing demographic policy, the state has enshrined in the tax legislation a kind of benefit: a tax deduction for personal income tax for children. Why is personal income tax or income tax taken? Because this is exactly the obligation that almost all citizens fulfill before the state. Russian Federation with the exception of pensioners - no income tax is withheld from the pension.

Application for a tax deduction for children: sample

Like all other benefits, the provision of tax deductions is carried out exclusively through an application from the applicant. It must be written to the accounting department of the enterprise where the parent is officially employed. The tax deduction is equally granted to both the father and the mother in a single amount established by the tax legislation. If the child is raised by one parent, then the deduction based on the submitted application will be provided in double the amount.

A standard sample application for a tax deduction for children can be obtained from the accounting department. Otherwise, the application can be made in free form, indicating the following details and personal data:

- the name of the enterprise (tax agent) where the parent works;

- surname, name, patronymic of the parent;

- surnames, names, patronymics of children for whom a tax deduction should be provided;

- children's age;

- for students over 18 years of age - the name of the educational institution in which the child is studying on a full-time basis;

- date and signature of the applicant.

Attention! Applications for granting a deduction are written annually! There is no deduction for a child over 24, even if they continue to study full-time!

Supporting documents

The application must be accompanied by a package of supporting documents for the tax deduction for children. These will be:

- photocopies on paper of the birth certificates of all children;

- for students over 18 years of age - the original certificate from educational institution which the child visits;

- a copy of the death certificate of the spouse (for single parents raising children). Single mothers of supporting documents about marital status not required - information about him was provided to the employer (tax agent) during employment;

- if any of the children has a disability - the original certificate from doctors about its presence.

How much will the benefit be?

The deduction sizes are different:

- for the first and second child - monthly 1400 rubles per child for each parent;

- for the third and all subsequent children - monthly 3,000 rubles per child for each parent;

- if the child has a disability - monthly at 12,000 rubles until he turns 18 years old. If he studies full-time, then up to 24 years;

- if a child with a disability is adopted, then monthly at 6,000 rubles.

I would like to point out that these tax incentives are provided not only to biological parents, but also to any legal representative: guardian, foster parent, adoptive parent.

In order to determine the amount of the deduction for the second or third child, do not forget that all born and adopted children are taken into account, regardless of age. If the oldest of the three children is already 25 years old, then who, for example, is 16 years old, will be provided in the amount of 3,000 rubles. Therefore, it is important for the applicant to list all children (regardless of age) in the application for the child tax credit. A sample of such information may not contain.

Finally

So, summarizing all of the above, we note the following:

- The tax legislation provides certain benefits to families with children.

- Sample applications for a tax deduction for children can be taken from the accounting department or found independently on the Internet.

- All children must be listed on the application to qualify for the exemption.

In any organization, for sure, there are employees who are entitled to standard personal income tax deductions. Because, as a rule, many employees have minor children. Therefore, it is not necessary to withhold tax from a certain part of the income of such workers, of course, if they ask for it. Therefore, the main thing for an accountant is to get a correctly executed application for a personal income tax deduction.

Look closely at the data in the table below. It shows in which case and in what amount the deduction is due. There may also be a situation if one of the employees has recently acquired housing and wants to take advantage of the property deduction at the place of work. The amount of such deduction for personal income tax also reduces the taxable income of the employee.

Standard deductions apply to the following categories of citizens:

- Disabled.

- Citizens with children.

- Military personnel.

This type of deduction is different in that it is due to the person's belonging to a particular category, in relation to which they are applied. More information is provided in the following table.

to the menu

The size of the standard deduction depending on the categories of payers

| Who gets the standard deduction | Size of the standard deduction, rub | Copies of documents required from the employee |

|---|---|---|

| Employees affected by the disaster at the Chernobyl nuclear power plant or in the work to eliminate the consequences of the accident, and some other employees listed in subparagraph 1 of paragraph 1 of Article 218 tax code RF | 3000 | Certificate of a participant in the liquidation of the consequences of the accident at the Chernobyl nuclear power plant, certificate of disability, etc. |

| Disabled since childhood, groups I and II, employees who received radiation sickness or other diseases associated with radiation, and other employees listed in subparagraph 2 of paragraph 1 of Article 218 of the Tax Code of the Russian Federation | 500 | Certificate of disability, certificate of a participant in the liquidation of the consequences of an accident at the Mayak production association, etc. |

| Parent of first or second child under 18 or full-time student under 24 | 1400 | |

| parent of a third or any next child under 18 or full-time student under 24 | 3000 | Child's birth certificate |

| Parent of a disabled child under 18 years of age or a full-time student of a group I or II disabled person under 24 years of age | 3000 | Birth certificate of the child, Certificate of disability. |

The aforementioned deductions are only possible if the employee will write a statement in his own hand. But, unfortunately, many citizens do not know about this opportunity or simply let everything take its course.

In order not to fall into unpleasant situation and not subsequently engage in proving your own innocence, we suggest that you familiarize yourself with the sample applications for deduction.

to the menu

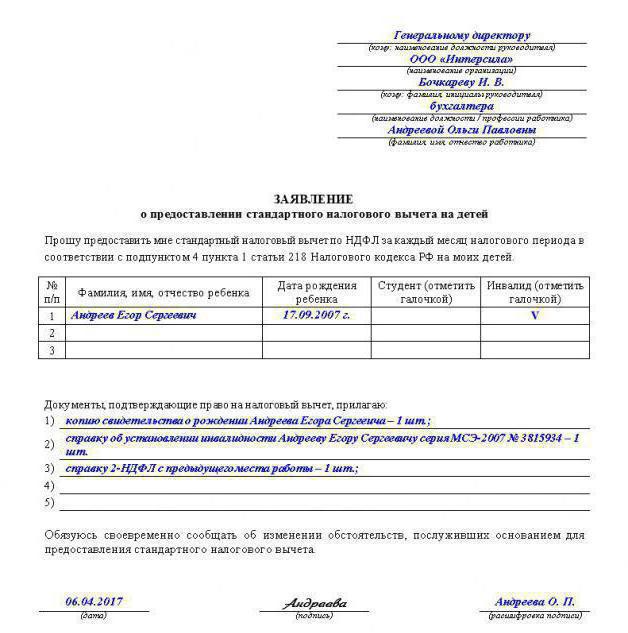

Application for the Standard Child Deduction

As you can already understand from the table of contents, it is provided if the employee has children. This is the most common case when an employee has children and wants to receive a standard personal income tax deduction. That is, use the right granted by subparagraph 4 of paragraph 1 of the Tax Code of the Russian Federation. In this case, an application from the employee is required, give him the application form for the standard deduction for children. An example of such a statement is shown below.

Ivanov I.I.

from the manager Lukyanova T.A.

STATEMENT

about the provision of a standard deduction

From April 2014, on the basis of subparagraph 4 of paragraph 1 of Article 218 of the Tax Code of the Russian Federation, I ask you to provide me with a standard personal income tax deduction for my first child, Dmitry Vladimirovich Lukyanov, who was born on April 19, 2014.

I enclose a copy of the child's birth certificate with the application.

Manager ___________T.A. Lukyanova

Do not forget that the standard personal income tax deduction is provided from the month of birth of the child.

note

in the application for the deduction, you do not need to put the year for which the employee asks for the standard deduction for the child. The amount of the deduction also does not need to be set, because in next year he may already be different and in this case he will come again to collect applications. Why do extra work. It is enough to receive it from an employee once (letter of the Ministry of Finance of Russia dated August 8, 2011 No. 03-04-05 / 1-551).

to the menu

Application for Double Standard Child Deduction

Double the standard deduction is due to employees who are single parents. For the first and second child, 2800 rubles are provided monthly, and for the third and younger children - 6000 rubles each month.

Be careful in this case., it is important to find out if the worker is actually a single parent. If this is not the case, after all, the deduction for the child will be increased illegally, which means that there will be an underpayment of personal income tax to the budget.

An employee is considered to be the only parent if the other parent is no longer alive or is not included in the child's birth certificate. The following situation is also possible - the second parent is entered in the birth certificate according to the mother. In this case, to confirm the right to a double deduction, you should bring a certificate from the registry office in the form No. 25, which was approved by Decree of the Government of the Russian Federation of October 31, 1998 No. 1274)

A sample application is provided below:

General Director of OAO "GASPROM"

Ivanov I.I.

From the cashier Nikolaeva A.A.

STATEMENT

on the provision of standard deductions for personal income tax

double as single parent

Please provide me with double the standard personal income tax deduction for my first child, Sergey Alekseevich Nikolaev, who was born on May 25, 2014.

Reason: subparagraph 4 of paragraph 1 of Article 218 of the Tax Code of the Russian Federation.

I confirm that I have been notified that I will lose the right to double deduction as a single parent from the month of marriage.

Cashier ____________ A.A. Nikolaeva

Keep in mind that on double standard tax deduction only unmarried persons can count. Upon marriage, an employee can receive a tax deduction only in a single amount. In this case, it does not matter whether the second spouse began to draw up parental rights on a child. Warn the employee about this and let him write it in his application for the deduction. It is recommended to warn the employee about this when he writes the application for the deduction.

There is also such a mistake, the divorce of an employee does not mean that he has become a single parent. Such an explanation is contained in the letter of the Ministry of Finance of Russia dated January 30, 2013 No. 03-04-05 / 8-78. Therefore, divorced parents do not receive a double personal income tax deduction for a child.

to the menu

Application for the other spouse to be entitled to a child deduction

The Tax Code of Russia also provides for such a scenario when one of the spouses refuses his deduction in favor of his spouse and if he has income that is taxed at a 13 percent rate, which he can confirm. These conditions do not apply to unemployed parents.

Sample application:

General Director of OAO "GASPROM"

Ivanov I.I.

from the accountant Kuznetsova A.I.

STATEMENT

about the provision of a standard deduction

including for the second parent

From January 2014, on the basis of subparagraph 4 of paragraph 1 of Article 218 of the Tax Code of the Russian Federation, I ask you to provide me with a standard personal income tax deduction for my first child, Kuznetsova Tatyana Aleksandrovna, born on May 20, 2012.

Attached to the application:

- a copy of the child's birth certificate,

- spouse's application for waiving the standard personal income tax deduction,

- a certificate from the spouse's work stating that he works at Planet LLC.

Accountant _________ A.I. Kuznetsova

Let us dwell in more detail on the amount of the deduction that is due to an employee whose spouse refused the deduction. For example, the husband refused the deduction in favor of his wife. This is her first child, which means the deduction is 1400 rubles. And the husband has two more children from his first marriage, which means that his deduction will already be 3,000 rubles. Therefore, the wife's deduction will be equal to the sum of these two deductions, namely 1400 + 3000 = 4400 rubles.

Pay attention to this

The income of an employee who wrote an application for a personal income tax deduction for a child does not exceed 280,000 rubles, and his wife has already exceeded this limit. Can he get a deduction for his wife?

No, he can not. After all, the spouse no longer has the right to a deduction, since her income has exceeded the limit. Because spouses are one whole, they have everything together: children, including income and deductions.

An employer who provides a parent of a child with a double personal income tax deduction for children must make sure that the other parent is entitled to the deduction (his income did not exceed 280,000 rubles), but does not receive this deduction. To do this, it is necessary that the parent claiming the double deduction submit a monthly certificate to his employer from the other parent's place of work. If the company did not require such certificates, it violated the conditions for granting a double deduction.

Note: On the need for monthly submission of certificates from the place of work of the second parent, see letter of the Ministry of Finance dated 03/21/12 No. 03-04-05 / 8-341.

to the menu

Application for property deduction

It represents the part of the amount that was spent by the employee on the purchase of housing, by which his income can be reduced. The right to such a deduction is noted in subparagraph 2 of paragraph 1. An employee can declare it if he contacts tax office or in the accounting department of the organization in which he works.

This is the situation, the employee wants to receive a property deduction in the organization, provides a notification from the tax that he has the right to a property deduction, and asks to provide it on a monthly basis. In this case, it is necessary to take an application for a deduction from the employee. Let's not forget that any deduction is available only upon application! Submit the form below to him.

Important! Make sure the notification is on the right this year. Because to assert your right to specific amount The employee must deduct every year. Compare the full name of the employee with the full name in the notification, this will not hurt, it is better to play it safe. Even when he receives a deduction for his spouse (there is such a right). If the data diverges, do not provide the deduction until the employee brings a properly formatted notice.

Sample application for a property deduction

General Director of OAO "GASPROM"

Ivanov I.I.

from the manager Sergeev A.P.

STATEMENT

about granting property deduction

I ask you to provide me with a property deduction for personal income tax from January 2014 on the basis of paragraph 2 of subparagraph 1 of Article 220 of the Tax Code of the Russian Federation.

Attached to the application is a notice from the Federal Tax Service No. 125 dated February 14, 2014.

Manager ___________ A.P. Sergeev

The deduction will be given as follows. Until the employee's income, taxed at a 13 percent rate, exceeds this amount, the tax will not need to be withheld.

If you mistakenly calculated personal income tax, having already received a notification from the employee, then at the end of the year the employee retains the overpayment. Then, according to the rules, it will have to be returned.

If the amount of the deduction indicated in the notice is more than the employee's income, then in this case the employee should contact the Federal Tax Service Inspectorate, where they will recalculate the balance of the deduction and issue a new notice for the next year.

to the menu

Deductions for children are included in the list of standard tax deductions for personal income tax. The right to such a deduction is regulated by Chapter 23 of the Tax Code of the Russian Federation, namely Article 218.

If a individual works for hire and has an employment relationship with the employer, then he needs to apply for a deduction at the place of work. If a citizen belongs to the category of the self-employed population, and at the same time he receives income taxed at a rate of 13%, then he will have to receive a deduction by filing a declaration with the tax office.

Who Can Apply for the Child Benefit

This is a personal income tax benefit, the basis for which is the presence of children. The deduction is granted for each child until they reach the age of majority, and in the case of full-time education up to the age of 24. You can get a benefit only if you receive income taxed at a rate of 13%. The following have the right to use the deduction:

- each parent;

- Adoptive parent;

- Spouse or wife of the adoptive parent;

- guardians;

- Trustees.

A single parent has the opportunity to reduce the tax base for personal income tax for a double deduction. This right remains until the moment of marriage, or until the child reaches the age of 18 or 24 if he is studying full-time.

The income limit for receiving a standard benefit for children is 350 thousand rubles. The tax base is calculated on an accrual basis from the beginning of the period. Moreover, if a citizen did not get a job from the beginning of the year, then he attaches a certificate from the previous employer to the deduction application.

If one parent is not receiving income, they may assign their child benefit entitlement to another. To do this, it is necessary to attach a written refusal of the spouse and a certificate of absence of income to the application for a tax deduction for children.

The standard deduction for a child is provided from the moment of birth (adoption, establishment of guardianship, guardianship) until:

- the end of the year in which the child turned 18 or 24;

- the moment of the child's marriage.

The duty of the employee is to notify the employer of the occurrence of one of the listed facts that cancels the standard benefit.

Do I need to submit an application every year?

The law provides that the benefit income tax provided by the employer after receiving an application for a standard tax deduction from the employee. An individual must show the initiative to receive the due benefits at the time of employment.

If the employee has started labor function not from the beginning of the year, but later, then the application for the deduction for the child is submitted from the date of employment, but is provided from the beginning of the tax period. This opinion is expressed by the Ministry of Finance.

The situation when the employee did not submit documents confirming the right to the deduction can be corrected. You can return the overpaid personal income tax from the budget by sending a 3-personal income tax declaration to the tax office. The declaration is submitted annually by April 30 of the year following the reporting year until the termination of the right to receive benefits.

The Tax Code of the Russian Federation does not provide for the annual filing of an application for a deduction for children. But the employer's accountant may require a rewrite of the document in the following cases:

- if the standard deduction application form specifies the year in which the benefit is to be granted;

- if the application form for a standard deduction provides for an indication of the amount of the benefit, and its amount has changed.

To avoid rewriting the application and collecting a package of documents, the employee can write an open-ended application.

How to write an application for a tax deduction for a child

The application form for a tax deduction in 2018 is arbitrary. Usually the employer provides a form in which the employee enters his data. But if ready template No, the application must include:

In the application header:

- The position of the responsible person of the employer;

- Name of the employer's organization;

- Name of the responsible person to whom the document is addressed;

- Position (profession) of the employee;

- Name of the employee.

The main part should contain:

- Name of the document (application);

- An employer's request for a standard tax credit;

- Reference to legislation (for example: Art. 218 of the Tax Code of the Russian Federation);

- Indication of the number of children and their full name and year of birth;

Applications:

- Copies of birth certificates for each child;

- Certificate from the educational institution;

- Certificate of medical and social examination (to confirm the disability of the child);

- Certificate 2-NDFL from the previous place of work (when applying for a job not from the beginning of the year).

Date and signature of the employee.

It does not matter how the application is written, handwritten or typewritten.

Sizes of standard deductions for children in 2018:

- First and second child - 1400 rubles;

- The third and subsequent - 3000 rubles;

- A disabled child for an adoptive parent, guardian, trustee - 6000 rubles;

- Disabled child for parents - 12,000 rubles.

All deductions must be presented to each of the parents (adoptive parents, guardians, trustees).

Depending on the situation, the following documents will be required to prove eligibility for the standard benefit:

- Birth certificates of children;

- Marriage registration certificate;

- Refusal of the spouse (wife) in case of assignment of the right to receive a deduction;

- Adoptive parents, guardians and custodians provide documents confirming adoption, establishment of guardianship or guardianship;

- Death certificate of the other parent;

- Court decision in case of establishing paternity (maternity) in court;

- Certificate from the educational institution on enrollment in full-time students;

- The conclusion of a medical examination when establishing disability, if necessary, to confirm the status of a disabled person, a certificate is provided to the employer with the frequency of its renewal;

- from the previous place of work, if employment does not occur at the beginning of the tax period.

Application for a tax deduction for a child in 2018 (sample)

The application for a standard child tax credit does not have an officially approved form, therefore it is made in free form. Here are some sample applications, following the example of which you can draw up your documents.

Application for child deduction

Take three applications for personal income tax deduction from employees

Since January, standard child income tax deductions have increased.

Give children's deductions according to the new sizes

An important detail - If the child is disabled, summarize the child deductions.

Last year, employees were eligible to receive children's standard deductions as long as their income from the beginning of the year did not reach 280,000 rubles. ( sub. 4 p. 1 art. 218 Tax Code of the Russian Federation). From January 1, 2016, this threshold has been increased to 350,000 rubles.

In addition, the child deduction for disabled children has quadrupled: from 3,000 to 12,000 rubles. per month. For guardians, trustees and foster parents the amount is doubled - up to 6000 rubles. The rest of the values remain the same. We have shown the sizes of all children's deductions in the table on this page.

If the child is disabled, the deductions must be summed up (letter of the Federal Tax Service of Russia dated November 3, 2015 No. SA-4-7 / 19206).

A company employee has three minor children, one of whom is disabled. Let's consider two situations.

Situation 1: a disabled child is second in a row.

An employee is entitled to the following child income tax deductions:

— 13,400 rubles. (1400 + 12,000) - for a second disabled child;

— 3000 rub. for the third child.

The total amount of the deduction is 17,800 rubles. (1400 + 13400 + 3000).

Situation 2: the third disabled child.

An employee is entitled to the following child income tax deductions:

- 1400 rubles. - for the first child;

- 1400 rubles. - for the second child;

— 15,000 rubles. (12,000 + 3,000) - for a third disabled child.

The total amount of the deduction will be the same - 17,800 rubles. (1400 + 1400 + 15,000).

Employees are now entitled to apply to the company for social deductions. And on property deductions, new clarifications that are beneficial for employees have been released. So, it's time to update the application forms for all three deductions.

Child benefit application

The standard deduction for a disabled child has increased from 3,000 rubles. up to 12,000 rubles (signature 4, clause 1, article 218 of the Tax Code of the Russian Federation). Redo the claims for child deductions if the old amounts are there. Also, new statements will be needed if the previous ones mention 2015.

It is better not to specify in the application the year for which the employee is asking for a deduction. This will save you from having to collect applications every year. But the size of the deductions should be given to avoid confusion. If they change in 2017, the statements will need to be updated.

Application for social security

Since 2016, employees can receive a social deduction for treatment and training not only in the inspection, but also from the employer (clause 2, article 219 of the Tax Code of the Russian Federation). The second option is more profitable because you do not have to wait until the end of the year to claim the deduction. But there is also a drawback: you need to get a notification from the inspection about the right to a deduction and only then apply to the company with a statement. The notification form for a social tax deduction was approved by order of the Federal Tax Service of Russia dated October 27, 2015 No. ММВ-7-11/473.

It is necessary to reduce the employee's income for a social tax deduction from the month in which he brings the notification and writes an application (clause 2 of article 219 of the Tax Code of the Russian Federation). It is not necessary to require documents confirming expenses from him.

If an employee regularly spends money on treatment and training, then he can apply for a notification at least every month. The inspection will issue a separate confirmation for each appeal. Another option for an employee is to accumulate expenses and receive a notification for all expenses of the year at once. The maximum amount of social tax deduction for yourself is 120,000 rubles. in year. If the employee paid for the education of his children, then the amount of the deduction is not more than 50,000 rubles. for each child in the total amount for both parents.

.

Application for property deduction

At the end of 2015, the tax authorities finally officially agreed that the property deduction must be provided to the employee for the entire year. When this employee brought a notification from the inspection, it doesn’t matter ( letter of the Federal Tax Service of Russia dated November 3, 2015 No. SA-4-7 / 19206). Previously, inspectors required the company to count deductions only from the month in which the notice was received. But now property deduction claims can be tweaked to benefit workers.

The maximum amount of the property deduction is 2,000,000 rubles. The amount of the deduction for interest on mortgage loans cannot exceed 3,000,000 rubles. To receive it, you only need a notification and an application. The notification form was approved by order of the Federal Tax Service of Russia dated January 14, 2015 No. ММВ-7-11/3. When the worker brings it to you, check if everything in it is correct. First, make sure the notice is for 2016. After all, the employee must confirm his right to a specific amount of the deduction every year. Secondly, the document must indicate the full name. employee and the name of your company.

.