Sample filling km 7 with acquiring. Is it necessary to apply the forms of primary documentation for accounting for cash settlements with the population when carrying out transactions using online cash registers. General filling rules

Form KM-7 is a daily filled out document that records the readings of cash registers. Refers to the primary documentation of the enterprise. Reporting is carried out by the senior cashier on the basis of type certificates. Data in the fields should be entered at the end of each business day after the Z report has been submitted. If you follow the letter of the law, then the finished form, as well as the reports attached to it, should fall into the accounting department no later than the next business day.

KM-7 does not have to be filled in manually. The main thing is that the report be printed on 2 sides and certified by the signatures of responsible persons.

Regardless of the number of cars, only 1 report on this form is issued per day.

Sample filling and blank form KM-7

FILES

Filling in the fields of the KM-7 form

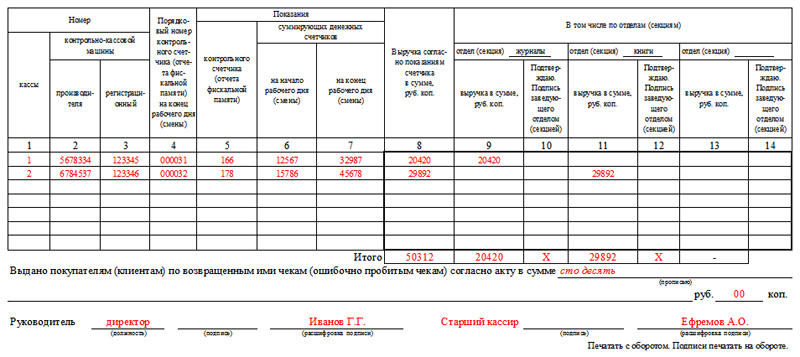

The header should contain the details of the company. In this case, the name may be incomplete, and the structural unit may not be indicated. The numbering of the form is set by the enterprise. It maintains the end-to-end order even after the change of the calendar year, i.e. if on December 31 it was KM-7 No. 342, then on January 1 it will be No. 343, and not No. 1, as one might assume.

Hat KM-7

The KM-7 cap can be said to be filled in in a standard way. The organization's data, name, address, and all its digital characteristics are entered:

- The table necessarily includes KKM numbers, which are entered in columns 2 and 3.

- The value for column 2 can be clarified in the passports of cars, and 3 - in documents from the tax office regarding the registration of cash equipment.

- In column 4, the number Z of the report is entered. Entrepreneurs are familiar with such cases when, after removing this report, they had to open the cash desk again and carry out operations. If this happened, in the fourth column we indicate the number of the last Z report.

- Revenue for the day (columns 8-14) is posted by sections. If the unit has more than 3 sections, you should fill out several forms.

- In boxes 10, 12 and 14, section leaders will need to sign to confirm that the information entered is correct.

If the enterprise does not have departments, columns 9-14 remain blank.

At the bottom of the form, the amount of returns on checks per day is filled in, including those that were broken by mistake. The number is entered in words, without duplicating numbers. Only the amount that buyers received in cash is entered in the field. Cash returns are not taken into account.

We remind you that the KM-7 form is submitted in a single copy per day. If during the inspection the tax inspector discovers the absence of a document, fines will be imposed on the company and the responsible person.

When the KM-7 form is not needed

The peculiarity of KM-7 is that it is a consolidated form. Thus, enterprises using no more than one cash register do not need to fill out such a report.

At the same time, maintaining such documentation is mandatory for all enterprises with cash registers, even if they do not specialize in commodity activities or operate according to a simplified scheme.

In what cases are organizations required to fill out the KM-7 form, and in which not? For example, enterprise No. 1 has a main cash desk and an operating cash desk. There is one cash register in the operating cash desk. Every day, the cashier-operator hands over the proceeds to the cashier of the main cash desk of the enterprise. The cashier-operator hands over to the cashier of the main cash desk KM-4, fiscal reports. Does the cashier of the main cash desk of the enterprise need to fill out the KM-7 certificate in this case? If a second KKM appears at the enterprise, how are things going with the KM-7 certificate? The second example: enterprise number 2 has a separate division. in a separate subdivision there are 2 cash desks: an operating cash desk (cash desk with the 1st cash register) and the main cash desk of the enterprise. The cashier-operator and the cashier of the main cash desk of a separate subdivision are one and the same person. Every day, the cashier credits the proceeds to the main cash desk of a separate subdivision, and the next day he delivers the proceeds to the cashier of the head unit for the previous day according to cash settlement. Does KM-7 fill in this case? If another 1 KKM appears in a separate subdivision, is it necessary to issue KM-7?

According to the Instructions (Decree of the State Statistics Committee of Russia dated December 25, 1998 N 132), form N KM-7 is used to compile summary report on meter readings of cash registers and the organization's revenue for the current working day and is an annex to the cashier-operator's Certificate-report for the current date.

The concept of "summary report" implies the presence of several objects that are subject to reporting. In this case, it is CCT. Thus, if an enterprise or a separate subdivision has several cash registers (more than one), form KM-7 must be filled out.

At the same time, form N KM-7 refers to documentation related to the use of cash registers in accordance with the Law on CCP. And, therefore, its failure to present it to the tax authority during an audit can lead to an administrative fine under Art. 19.7 of the Code of Administrative Offenses of the Russian Federation:

For officials - from 300 to 500 rubles;

For legal entities - from 3000 to 5000 rubles.

Thus, for both the first and second examples, the need to fill out the KM-7 form will appear only when another KKM is installed.

The rationale for this position is given below in the materials of the Glavbukh System

The use of CCP is associated with the execution of various primary documents.

End of shift

At the end of the work shift, the cashier-operator:

- on the basis of the Z-report, makes entries in the journal of the cashier-operator in the form No. KM-4;

- draws up a certificate-report of the cashier-operator in the form No. KM-6. This document also reflects the readings of control and totalizing meters, the amount of revenue per shift and the amount of money returned to customers. The report is drawn up in one copy and, together with the proceeds, is transferred to the main cash desk.

- returns to the senior cashier of the main cash desk the amount of money received at the beginning of the shift for exchange and initial settlements with customers. This return is recorded in the ledger of funds received and issued by the cashier in the form No. KO-5. In confirmation of the return of this amount, the senior cashier signs in column 9.

This procedure is provided for in clause 6.1 of the Model Rules approved by the letter of the Ministry of Finance of Russia dated August 30, 1993 No. 104, clauses , 4.5 of the Bank of Russia instruction No. 3210-U dated March 11, 2014, instructions for filling out forms No. KM-4 and No. KM- 6, approved, instructions for filling out the form No. KO-5, approved by the Decree of the State Statistics Committee of Russia dated August 18, 1998 No. 88.

Based on the certificates-reports of cashiers-operators, the cashier (senior cashier) draws up a summary report for all cash registers (form No. KM-7 "Information on the readings of counters of cash registers and the organization's revenue"). It is made in one copy. Columns 5-7 of the summary report reflect the readings of the meters of each KKM, column 8 - the amount of revenue. Separately, it is indicated how much money was given to buyers when returning goods and what amounts were entered by mistake. The summary report is signed by the senior cashier and the head of the organization. It is transferred to the accounting department along with receipt and expenditure orders and certificates-reports of cashiers-operators. This procedure is provided for by the instructions approved by the Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132. *

Elena Popova,

State Advisor of the Tax Service of the Russian Federation of the 1st rank

2. Article:What cash registers need to be kept

Is it required to maintain forms KM-6 “Reference-report of the cashier-operator” and KM-7 “Information on the readings of KKM meters and the organization's revenue”?

From January 1, 2013, the forms of primary accounting documents contained in the albums of unified forms of primary accounting documents are not mandatory. This follows from Article 9 of the Accounting Act.

At the same time, this rule does not apply to state and municipal institutions.

They must use the forms of documents contained in the annexes to the order of the Ministry of Finance of Russia dated December 15, 2010 No. 173n. At the same time, forms No. KM-6 and No. KM-7 are not indicated there. Therefore, the current legislation does not formally oblige to fill out these forms after January 1, 2013.

However, the information of the Ministry of Finance of Russia No. PZ-10/2012 explains that the forms of documents used as primary accounting documents established by authorized bodies on the basis of other federal laws continue to be mandatory for use. For example, cash documents*.

On the one hand, the forms mentioned in the question do not apply to cash documents.

At the same time, these forms are used when carrying out tax and financial control measures. For an example, let's turn to paragraph 34 of the Administrative Regulations ... on the implementation of control and supervision over compliance with the requirements for cash registers ... approved by order of the Ministry of Finance of Russia dated October 17, 2011 No. 132n. According to it, in the performance of the state function, depending on the period under review and the specifics of cash settlements, inspection specialists consider, in particular, the journal of the cashier-operator, the certificate-report of the cashier-operator, as well as information on the readings of counters of cash registers and the organization's revenue *.

I.A. Kolodin,

budget accounting expert

primary accounting documentation for accounting for cash settlements with the population in the course of trading operations using cash registers were approved by the Decree of the State Statistics Committee of the Russian Federation dated December 25, 1998 No. 132.

When accounting for cash settlements with the population in the implementation of trade transactions using cash registers, the forms of primary accounting documentation No. KM-1, KM-2, KM-3, KM-4, KM-5, KM-6, KM-7 are used , KM-8, KM-9.

|

Form number |

Form name |

|

The act of transferring the readings of the summing money counters to zeros and registering the control counters of the cash register. |

|

|

The act of taking readings of control and summing cash meters upon delivery (sending) of the cash register for repair and upon its return to the organization |

|

|

Act on the return of money to buyers (clients) on unused cash receipts |

|

|

Journal of the cashier - teller |

|

|

Journal of registration of readings of summing cash and control counters of cash registers operating without a cashier - teller |

|

|

Help-report of the cashier - teller |

|

|

Information about the readings of counters of cash registers and the organization's revenue |

|

|

Logbook of technical specialists calls and registration of work performed |

|

|

Act on the verification of cash |

When commissioning new cash registers and when conducting an inventory in organizations to formalize the transfer of readings of totalizing counters and registering control counters (fiscal memory report) before and after their transfer to zero, the Act on transferring the readings of summing cash counters to zero and registering control counters is applied. cash register counters (form No. KM-1).

The conversion of the readings of the summing counters to zero and the registration of the control counters of the CCP is carried out in the presence of a commission, which must include a representative of the controlling organization or a representative of the tax department. The act is drawn up in two copies, one of which, as a control copy, is transferred to the organization servicing and controlling cash registers, the second copy remains in the organization.

The act is signed by the responsible persons of the commission, consisting of a representative of the controlling organization, the head, the chief accountant, the senior cashier and the cashier of the organization and records the readings of the following counters:

control counters (fiscal memory report);

registering the number of transfers of readings of the summing counters to zeros;

main summing counter;

· sectional totalizing cash counters.

When filling out the act, in the line "Number" / "Manufacturer" the number of cash register equipment indicated in its technical passport is affixed, in the line "Number" / "Registration" the number under which this cash register is registered with the tax department is indicated.

The reason for drawing up the act is indicated in the line "Basis".

When repairing cash registers by specialists of the technical service center and when transferring them for work to other organizations, for registration of taking meter readings, the Act on taking readings of control and summing money meters is applied when handing over (sending) the cash register for repair and returning it to organization (form No. KM-2). Repair of cash register equipment is carried out with the permission of the administration of the organization only after taking readings of summing cash and control counters (fiscal memory report).

The act is drawn up and signed by members of the commission, which, as in the preparation of the Act of the form No. KM-1, includes without fail a representative of the controlling organization or a tax representative, as well as the head, senior cashier, cashier of the organization and specialist of the CCP technical service center.

An invoice is drawn up for the transfer of cash registers to another organization or to a technical service center for repair. The act, together with the drawn up invoice, is submitted to the accounting department of the organization no later than the next day. Notes about this are made in the Journal of the cashier-operator (form No. KM-4) at the end of the entries for the working day.

After the repair, the meter readings are checked and recorded in the act, and the casing of the cash registers is sealed.

It is not uncommon for a buyer to refuse a purchase and turn to the administration of a trade organization with a demand to return the money to him. In this case, the head signs the check punched at the cash desk and allows the cashier to return the money to the buyer, while the money can only be returned according to the check punched at this cash desk and in the amount indicated on the check.

To issue a refund to buyers (clients) on unused cash receipts, including erroneously punched cash receipts, use Act on the return of money to buyers (clients) on unused cash receipts (form No. KM-3). The act is drawn up and signed in a single copy by the commission, which includes the head, the head of the department or section, the senior cashier and the cashier-operator. The act, which lists the number and amount of each check, together with canceled checks pasted on a sheet of paper, is submitted to the accounting department of the organization, where it is stored in documents for this number.

It should be noted that the amount of cash on checks returned by buyers (clients) is reduced by the cash register revenue and is entered in the Journal of the cashier-operator (form No. KM-4).

In all organizations that carry out cash settlements with the population using cash registers, the receipt and expenditure of cash for each cash register is taken into account. For this purpose, it is applied Journal of the cashier-operator (form No. KM-4), which in addition is also a control and registration document of meter readings.

The journal must be laced, numbered and sealed with the signatures of the representative of the tax authority, as well as the head and chief (senior) accountant of the organization and the seal. The journal keeps records of revenue received with the use of cash registers.

Entries in the journal are kept by the cashier-operator daily in chronological order with ink or a ballpoint pen. If errors are made when recording data in the journal, then the corrections made must be specified and certified by the signatures of the cashier-operator, manager and chief (senior) accountant of the organization.

If the readings match, they are entered in the journal for the current day or shift at the beginning of work and certified by the signatures of the cashier and the administrator on duty.

The date of the report is indicated in column 1, the readings of money counters at the beginning and end of the shift are recorded in columns 6 and 9, the total amount of revenue is indicated in column 10, the amount of cash handed over is recorded in column 11 of the journal, the amount of revenue from credit cards is indicated in column 12 "Paid according to documents".

Column 4 of the journal is provided to record the amounts issued on checks returned by customers, based on the data of the Act in the form No. KM-3, as well as the number of zero checks printed per working day (shift). At the end of the working day (shift), the cashier draws up a cash report, along with which, according to the receipt cash order, he hands over the proceeds to the senior cashier.

An entry in the journal of the cashier-operator is made after taking meter readings and checking the actual amount of revenue, the entry is confirmed by the signatures of the cashier, senior cashier and administrator of the organization.

In the event of a discrepancy between the results of the amounts on the control tape and the proceeds, the reason for the discrepancy should be clarified, and the identified shortages or surpluses should be entered in the appropriate columns of the Journal of the cashier-operator.

In many organizations that work without a cashier-operator (installation of cash registers on store shelves, for the work of waiters), to record cash receipts (revenues) for each cash register, a register is used for registering the readings of summing cash and control counters of cash registers working without a cashier-operator (form No. KM-5). Like the previous journal, it is also a control and registration document of meter readings and must be laced, numbered and sealed with the signatures of a representative of the tax authority, the head and the chief (senior) accountant of the organization and the seal.

Entries in the Journal are kept by a specialist working on a cash register, daily in chronological order after the end of the working day (shift) in ink or a ballpoint pen. The journal records the readings of the control and summing cash counters and the amount of revenue. Reception - delivery of funds is formalized by the signatures of a representative of the administration of the organization, a controller-cashier, a seller, a waiter and others. In case of discrepancies between the amount of actual revenue and the result of the amounts on the control tape, the reasons for the discrepancy are identified, the identified shortages or surpluses are entered in the appropriate columns of the journal.

If corrections are made to the journal, the corrections made are negotiated and certified by the signatures of the cashier, controller-cashier, seller or waiter, head and chief accountant of the organization.

Every day, the cashier-operator in one copy draws up a report on the readings of counters for cash registers and revenue for the working day (shift). Used to generate a report Help-report of the cashier-operator (form No. KM-6). The signed report, together with the proceeds from the receipt order, is handed over by the cashier-operator to the senior cashier or head of the organization. If the organization is small and one or two cash desks work in it, then the cashier-operator can deposit money directly with the bank collector. The transfer of funds to the bank is reflected in the report.

Revenue for a working day (shift) is determined by the readings of summing cash counters at the beginning and end of the working day (shift), while the amounts of money returned to buyers (clients) on unused cash receipts are deducted. The proceeds are confirmed by the signatures of the heads of departments, while the proceeds are accepted and credited to the cash desk on the basis of an incoming cash order, and the senior cashier and the head of the organization sign in the report.

Help-report of the cashier-operator is the basis for compiling a summary report Information on the readings of counters of cash registers and the organization's revenue (form No. KM-7). This report is compiled by the senior cashier on a daily basis and, together with acts, certificates, reports of cashiers-operators, receipt and expenditure cash orders, and is transferred to the accounting department of the organization before the start of the next shift. This form is a table in which, according to the meter readings at the beginning and end of work, revenue is calculated for each cash register and distributed by departments, which is confirmed by the signatures of the heads of departments (sections). The results of the meter readings of all cash registers and the organization's total revenue with its distribution by departments, as well as the total amount of money issued to customers on the cash receipts they returned, are summed up at the end of the table. The form is signed by the head and senior cashier of the organization.

In the event of a breakdown of the cash register, if it is impossible to eliminate the malfunctions by the cashier, the administration calls a specialist in the maintenance center for cash registers. Also, the specialists of the technical service center conduct scheduled technical inspections, during which the condition of the mechanisms of the electronic and software parts of the cash register is checked, and minor malfunctions are eliminated.

In organizations, to reflect these facts, they use Log book for calls of technical specialists and registration of work performed (form No. KM-8). The journal is kept by the head of the organization or his deputy, but is maintained by a technical center specialist who makes records of the work carried out, in particular, the sealing and the content of the brand imprint. If it is necessary to repair the cash register at the technical service center, this is reported to the management of the organization and a corresponding entry is also made in the log, which is confirmed by the signatures of the specialist of the technical service center and the responsible person of the organization on the acceptance of work on the repair of CCP.

Form KM-7 is a document that is directly related to the use of cash registers with ECLZ. The obligation to use it was canceled from July 2016 with the amendment of the law "On the use of cash registers" dated May 22, 2003 No. 54-FZ. And since July 2017, this form has generally become unnecessary due to the cessation of the use of cash desks equipped with ECLZ. However, this does not prevent the continuation of the use of the KM-7 form only insofar as it relates to information about the amount of revenue received per shift.

About what technique replaced KKM with EKLZ, read the article "The procedure for the transition to online cash registers from 2016" .

During the use of cash desks equipped with ECLZ, the KM-7 form was a mandatory annex to another unified form - KM-6, which was supposed to be a cashier-operator. But with the introduction of amendments to the law "On the Application of KKM", the KM-6 form is filled out only at the request of the economic entity.

The report in the KM-7 form provides columns for indicating the factory, as well as registration numbers of all used cash registers. Moreover, it was required to form it for any number of cash registers available, including for a single cash register.

The form of the KM-7 form was approved by the Decree of the State Statistics Committee of the Russian Federation of December 25, 1998 No. 132. You can download it on our website.

What are the features of filling out a report in the KM-7 form

Form KM-7 was to be generated daily in 1 copy and handed over to the accounting department before the start of the next work shift together:

- with form KM-6;

- PKO, RKO;

- acts in the form of KM-3 (for the return of money to buyers).

The table, which is the main element of the KM-7 form, indicated and summarized the indicators for all fiscal counters of the CCP, as well as for cash proceeds for the trading entity as a whole or broken down by departments (in this case, the figures were certified by the signatures of the heads of the relevant departments).

The amounts reflected in the acts in the KM-3 form, that is, returned to the buyers of the company, were indicated in words in a special column located under the table.

The information recorded in the KM-7 form was certified by the head of the trading entity, as well as by the senior cashier.

Read about the KUM-3 form in the material

The work of a cashier is not only in receiving and issuing cash, but also requires competent execution of cash documentation. One of these documents is the KM-7 form - Information on the readings of KKM meters. This report is compiled by the cashier-operator and accompanies the closing of the working day on the fiscal apparatus of cash registers.

A form of information on the readings of KKM meters form KM-7 and a sample filling can be found in the article below.

The report records the totals of the work shift - information of counters, amounts and other information reflecting cash accounting.

Form KM-7 is also used as a basis document for compiling a consolidated report on all cash registers, if there are several of them in the organization. At the same time, the KM-7 form shows data on a specific cash register at the end of the day.

The completed sample of information is handed over by the cashier to the accounting department along with orders, return acts (we suggest downloading the PKO sample for free, the RKO sample - in).

The organization must remember that the new KKM requires mandatory registration with the tax office, and you need to fill out. The same statement is required when you need to make changes to an existing CCP or remove it from the register.

The procedure for filling out the KM-7 form

Filling in information about meter readings is performed on the basis of ready-made report forms for cashiers-operators. Form KM-7 is attached to cash reports.

Filling instructions:

- the details of the organization, the owner of the cash register are filled in;

- the name of the department is indicated;

- the number is affixed, as well as the date of registration to the nearest minute;

- in the "attachment to cash reports" field, list all cash reports for which the combined form KM-7 is drawn up;

- information about the serial and registration number of the cash register is filled in the table;

- further, the readings of the KKM counters are entered, at the beginning and end of the shift;

- followed by the total revenue per day, divided by department and in the total amount;

- signatures of cashiers - are placed opposite the amount of revenue;

- the amount returned to buyers according to the act is separately noted.

A completed sample of information on meter readings form KM-7 must be signed by the following persons.